|

| Telco 2.0: The findings of the 18th Telco 2.0 Executive Brainstorm, part of the New Digital Economics EMEA event, held in London 12-13 June. This event was designed to drive market transformation, encompassing new forms of voice & messaging for the digital consumer, customer experience management, and the future of telecoms operators’ networks. |

|

Part of the New Digital Economics Executive Brainstorm series, the 18th Telco 2.0 event took place at the Grange St. Pauls Hotel in London on the 12th June. It looked at the shape of the digital economy, the role of major platforms, the future of voice, managing multi-channel customer relationships, and the evolution of operator networks. The following day, STL Partners hosted dedicated events on Cloud 2.0, Digital Things 2.0 and Digital Commerce 2.0 in the same venue.

Using a widely-acclaimed interactive format called ‘Mindshare’, the event enabled specially-invited senior executives from across the communications, media, banking and technology sectors to discuss opportunities, challenges, and practical experiences.

For more information please contact: STL Partners (www.stlpartners.com)

Email: . Phone: +44 (0) 207 247 5003.

DOWNLOAD REPORT

With thanks to our Platinum Sponsors:

Table of Contents:

- Introduction

- Executive Summary

- Session 1 – The Market 2.0

- Stimulus presentations

- Voting, feedback, discussions

- Key takeaways

- Session 2 – Digital Consumer 2.0

- Stimulus presentations

- Voting, feedback, discussions

- Key takeaways

- Customer Experience 2.0: Deepening Relationships in a Fickle World

- Stimulus presentations

- Voting, feedback, discussion

- Key takeaways

- Network 2.0: (Re)Monetising Telcos’ Core Asset

- Stimulus presentations

- Voting, feedback, discussions

- Key takeaways

- About STL Partners

Table of Figures:

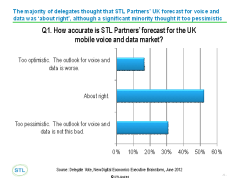

- Figure 1: The mobile service revenue gap in the UK market

- Figure 2: Will the UK mobile market contract by 24% by 2018?

- Figure 3: Understanding the key battlefields in the digital economy

- Figure 4: Strategic options for telcos

- Figure 5: Should telcos move independently or collaborate?

- Figure 6: Do strategies perceived as commoditisation = real growth?

- Figure 7: Are we trapped in a prisoners’ dilemma?

- Figure 8: Reorganising KPN for external innovation

- Figure 9: Cultural change at KPN

- Figure 10: Disruption in the SMS market.

- Figure 11: Responding to the disruption

- Figure 12: What telcos need to change

- Figure 13: Telcos are surprisingly relaxed about Skype

- Figure 14: Six strategic options in voice

- Figure 15: TU, an example of Telco 2.0

- Figure 16: The hierarchy of communications need – reach comes first?

- Figure 17: A case for RCS-e succeeding?

- Figure 18: The benefits of a good API

- Figure 19: Easypaisa – commerce is universal

- Figure 20: Telenor future priorities in Telco 2.0

- Figure 21: OTT voice and messaging – a must

- Figure 22: Collaboration is telcos’ number 1 option

- Figure 23: What percentage of your customers are advocates, antagonists, or apathetic?

- Figure 24: The fragmented future: eight VoIP apps on an iPhone

- Figure 25: Customer Experience Innovation strategies for Telcos

- Figure 26: Does the typical customer even exist?

- Figure 27: An MVNO with a Difference

- Figure 28: Operators don’t have a vision for customer experience

- Figure 29: Operators’ understanding of their advocates and antagonists is poor

- Figure 30: Operator analytics are deemed to be poor

- Figure 31: Ore to jewellery: the value chain

- Figure 32: Operators and upstream players are in agreement about APIs

- Figure 33: Operator positioning for API projects

- Figure 34: How to design a network monetisation programme

- Figure 35: Cisco view – integration of compute resources right into the network

- Figure 36: Operators as a central hub for content, enabled by authentication

- Figure 37: Telcos’ control points