Summary: As several operators in Europe downsize their Telco 2.0 Digital Services activity, some are seeking to reframe the Piper strategy as a premium-priced differentiation play based on network quality. This report argues this is deluded and dangerous – a Piper strategy is viable but only by developing cost-leadership in a commodity market.(June 2015, Executive Briefing Service)

Below is the full 13 page Telco 2.0 Report that can also be downloaded in PDF format by members of the Telco 2.0 Executive Briefing Service here.

For more on any of these services, please email / call +44 (0) 207 247 5003.

What is ‘Repremiumization’?

Promoted as a viable strategy recently at STL Partners’ Senior Executive Strategy Seminar in London…

Last week STL Partners held an event for senior strategists, marketers, and digital unit leaders across Europe. The event was attended by 24 executives from 13 operators and 5 executives from Cisco, Intel and CSG International. All except a handful of people held senior positions within the European telecoms industry – they were not junior staff but instrumental in shaping the thinking at some of the leading European operators.

The event covered several strategic issues facing the European and, in many cases, wider global telecoms industry including:

What will the structure of the European market look like in 2020? STL Partners presented four scenarios and asked attendees to vote on the most likely scenario as well as facilitating discussions. The scenarios will be presented in a report published this month (June 2015), Reading the Crystal Ball: The European Telecoms market in 2020.

Where and how should operators build value in the digital ecosystem? STL Partners presented the case for four strategic options for operators to compete (we will cover these in a forthcoming report in July 2015, Four strategic pathways to Telco 2.0:

Piper: An infrastructure-led, network-oriented strategy focused on moving bits and bytes efficiently and effectively while leaving service development and delivery to other players. Accept that Telco 2.0 equates to speedy and smart data pipes and focus on cost leadership now.

Content: Couple infrastructure capabilities with content distribution (especially video). Explore options that range from sophisticated content delivery networks all the way to content creation either via commissioning (Netflix model) or exclusive rights.

Enterprise: Accept that differentiation in the consumer segment is impossible but that operators have the skills and relationships to build an expanded role in the large and growing Enterprise ICT market.

Authentication: Building digital services has proved challenging for operators but authentication potentially presents a real opportunity to establish a new digital ‘control point’ for operators from which a viable services strategy –for B2B2C enablers and end-user services – can be established.

Winning approaches to building scaled telecoms digital initiatives. Operators from Europe and beyond presented case studies on their digital activities – focusing on what had worked well and what less well – and attendees discussed the merits and demerits of different approaches.

It was in the second session on how to build value in future that the notion of ‘repremiumization’ was articulated (although nobody used this term). In essence, participants from at least two Tier 1 telcos felt that STL Partners’ description of the Piper strategy as one of competing hard in a commodity market – a market characterised by lack of differentiation in services – was wrong and that in future they would be able to ‘reframe the value of the network in the minds of consumers’ by differentiating against other players based on network quality. This differentiation would enable them to attract premium prices and grow ARPUs. The well-trodden path of ‘network APIs’ were cited as a key way of driving additional volumes (and revenue) through a premium-quality network.

Indeed, attendees were so insistent that this ‘repremiumization’ strategy was viable that when STL Partners asked attendees to vote on the four strategic options (2.1-2.4 above), they asked for it to be added as a fifth option which we have termed ‘Premium Piper’ in Figure 1 below. The chart reflecting the votes of attendees, below, is interesting for a number of reasons:

Nearly two-thirds of attendees felt that a ‘Pipe’ strategy of some sort was the best for European operators. In other words, competing in the services layer was regarded as extremely challenging by many. This, one suspects, is due to the challenges European operators have had in launching digital services having pursued the strategy late (from 2009 onwards after the market for core voice, messaging and data services had already peaked) and, in most cases, in a half-hearted fashion.

Exactly half of those that selected a ‘Pipe’ strategy felt that STL Partners’ Piper was the better approach and the focus should be building great pipes while striving for cost leadership. The other half felt that a ‘Premium Piper’ strategy was more attractive and that differentiation could be achieve on a sustainable basis through network quality.

Those that did support a Europe-wide digital services (non-Piper) strategy were quite evenly split between Content, Enterprise and Authentication (with one person selecting ‘Other’) suggesting that a single non-Piper strategy for the whole European telecoms market is not obvious. (NB We presented the Service Options as single choices rather than ‘do all’ in order to crystallise the debate at the event.)

Figure 1: Where should the European telecoms industry place its bets for future success?

The notion of a superior network resulting in superior revenues and returns is one that has, for example, been put forward in a paper by Bain and Company’s European office – the argument is set out here and can be summarised thus:

Operators have chosen to compete on price and have thus ‘trained’ consumers to make price the main criteria for choosing an operator.

As prices have fallen, consumers have started to think of operators as mere providers of connectivity and networks as a commodity.

The focus on price has led to lower returns on investment in Europe and, consequently, less network investment.

Fortunately, there are markets (including the US) where customers pay a premium for great connectivity because they appreciate how important the network is to their digital lifestyle.

Therefore, operators must educate customers about how important their networks are and invest in them to realise a price premium as illustrated by this chart:

Figure 2: ARPU levels of 7 customer segments with and without better network services and digital ‘life experience’ offers

NFV and SDN will be key drivers of premium networks by enabling operators to, for example, dynamically increase speed or bandwidth.

Unlike the past when tier 2 competitors have easily been able to copy market leaders network improvements and so have commoditised the network, market leaders can now use their scale and marketing skills to establish a ‘perceptual shift’ in consumers.

There must be cross-functional developments at operators to deliver on the new ‘premium product’ market promise.

Why is repremiumization 100% hogwash?

STL Partners is convinced that repremiumization is wrong.

Let’s explain why.

The repremiumization argument simply does not stand up to scrutiny

Here is our challenge to the 8 point argument outlined above for repremiumization.

Operators have not chosen to compete on price. In fact, they have spent significant efforts trying to build and market differentiated brands and services. Going all the way back to 2002, mobile operators were building digital lifestyle offerings under brands such as Vizzavi, Vodafone Live!, Orange Dot, Genie, and so forth. Attempts to build differentiated services and brands that would enable them to attract more customers and/or achieve premium prices has been the main focus of marketing departments at every operator in Europe since they started out.

The attempts to differentiate have largely failed despite operators’ best efforts. The fact that operators are seen as ‘merely providing connectivity’ is illustrative of this failure and they have been forced, rather than chosen, to compete on price – falling prices are a product of a failed differentiation strategy that…

…has indeed resulted in gradually lower returns on investment as ‘excess profits’ have been competed away – something that happens in most markets and particularly in ones where there is healthy competition and differentiation is difficult to achieve – think commodities, utilities…

There are several reasons why customers pay premium for services in some markets. These include:

Market structure: a consolidated market with a high Herfindahl Index (an economists’ measure of market competitiveness) will tend to have higher prices than fragmented markets with a low Herfindahl Index as one or two large operators are able to exert pricing power.

Higher growth markets tend to have higher prices because operators do not need to compete so hard to grow. Winning customers is easier as new customers take the product for the first time. Conversely, saturated markets tend to display greater price pressure as operators are forced to drop prices to retain or win customers.

Regulation. In some markets the regulator creates a benign environment for operators by, for example, blocking VOIP which reduces the degree of substitution for traditional telephony. Markets like this again tend to ‘enjoy’ premium pricing.

The US market, cited by Bain, has enjoyed all three benefits compared with Europe. It has 4 mobile operators serving 300m subscribers (with two very large players in AT&T and Verizon and two much smaller ones in T-Mobile and Sprint) compared with 50+ in Europe serving a similar number of customers in total and with most individual European markets having more balanced and, therefore, competitive market shares. Mobile took off later in the US than Europe so the market has continued to grow over recent years while Europe has stalled. The FCC has, until recently, been relatively benign towards telcos despite the hoo-ha over the last 10 years’ around ‘network neutrality’. The European regulator has, by contrast, been pretty harsh on telecoms operators and, among several measures, mandated fixed and mobile price decreases and effectively abolished voice and data roaming charges.

What is interesting now is that prices in the US are in freefall. The US price premium is rapidly on its way out. The reason for this is more aggressive behaviour from T-Mobile and Sprint combined with lack of underlying market growth (the market has peaked) and a less supportive regulator. Repremiumization has been tried by Verizon and by AT&T but it simply will not work if competitors charge significantly less for a satisfactory data service.

The Bain chart does indeed suggest that price premium is possible in telecoms but this is for services not for bandwidth, prioritisation, and other network capabilities. ‘Better network offers’ suggest a negligible ARPU uplift so it would be a much better in point 6 to argue that…

…NFV and SDN will enable operators to cut operating expenses and capex and, potentially, speed up the delivery of new services. Yes, dynamically adapting the network to support services may enable service differentiation for some segments but the value will be associated with the service itself not the network delivering it so the ability for operators to differentiate solely via the characteristics of the network will be minimal.

Challengers cannot beat market leaders in terms of perceptions of quality? Huh? Are you serious? Why? What is different now? Tier 1 operators have always enjoyed scale and marketing spend advantages. If they have failed to differentiate their networks and brands in the past, then a ‘repremiumization’ marketing message won’t make the slightest difference.

We agree(!) that operators need cross-functional developments at operators to deliver new propositions and transform the core of their businesses.

Better networks are a source of advantage for operators by enabling cost leadership

3UK’s value-for-money strategy…

STL Partners does believe that operators with a network advantage do enjoy a competitive advantage. 3 in the UK illustrates this point nicely. It has gone from being a joke among consumers between 2003 and around 2010 owing to poor handsets and network quality, to being the network of choice for, as Bain's survey puts it, the ‘Digitally Powered’. Indeed it heavily markets its network based on its quality:

‘Big-boned’ ‘Designed for the Internet’ ‘More capacity than any other’

The message is that the 3 network is bigger, faster and better than rivals. So is this an example of differentiation and price premium based on network quality?

No.

3UK’s network, being younger than its peers, is more efficient – the company has a 3G and 4G network only and is not hamstrung by the expensive and complex patchwork of 2G networks that Vodafone, O2 and EE (T-Mobile and Orange) have to manage. This cost advantage has been further increased by an outsourcing strategy that has been in force for at least a decade – 3 was the first UK operator to outsource its network as well as most product development and management functions.

An efficient network has enabled 3UK to focus on offering better value than its peers to consumers. Its strategy of connecting over 90% of its base stations with fibre backhaul rather than microwave and its dubious ‘advantage ‘of having lots of spectrum for each subscriber compared with other players (owing to its historical low market share) also means that it is not capacity-constrained. Because it is has a lower cost base and lots of excess capacity, it can offer more data and speed for the same price as peers and still make more money than them.

This is not differentiation based on network capabilities – APIs, dynamically delivered bandwidth, etc. but simply a cost advantage that means that 3UK can deliver data more efficiently than others enabling it to offer better value to consumers and so pull away from its peers in terms of volume and margin growth (see Figure 3). It is interesting to note that 3UK is, like the cost-leader Free in France and Play in Poland, a late entrant not a big Tier 1 incumbent at all – quite the reverse of the argument put forward in Bain’s paper.

Figure 3: 3UK winning market share and growing margins against the three bigger players

Source: Company accounts, STL Partners/Telco 2.0 analysis

..does not equate to repremiumization…

Readers may be thinking that if 3UK is able to offer a better data service, then surely it could, if it chose to, price this at a premium and so lift ARPU and margins that way – surely network-based differentiation is alive and kicking?

No, STL Partners thinks that higher access and data prices for 3UK would be highly unlikely on a sustainable basis for two reasons:

Cost leadership does not equate to price leadership. In a price sensitive (commoditised) market like telecoms, having a lower cost base may enable you provide a marginally better product or service than competitors but this does not necessarily enable you to price it higher (see Lessons from the steel industry: Network quality is unlikely to provide sustainable differentiation below). 3UK may be able to offer more data to a subscriber than competitors (and so achieve a higher ARPU) but it will struggle to convert, for example, lower latency into a higher price.

Cost advantages are likely to be competed away. The other operators in the UK will be competing hard to lower their cost base to ensure that 3UK does not continue to enjoy an advantage. EE (itself a result of the need for lower costs by T-Mobile UK and Orange UK), for example, has agreed a deal to be acquired by BT (subject to regulatory approval) which will dramatically lower its backhaul costs. O2 looks likely to be snapped up by 3UK itself – the resulting entity is likely to have a cost base, at least for a few years, that is somewhere between the two companies'. These two moves alone may wipe out 3UK’s cost advantage and so jeopardise the value-for-money strategy. That is before we consider the financial impact on Vodafone UK’s recent £1billion investment in its network and potential partner/merger/acquisition of Liberty Global (owner of Virgin Media UK) or Sky.

…and will not yield ever-increasing ARPU

If 3UK is unlikely to achieve sustainably higher prices than competitors, surely rising demand from video and other consumer services and the Internet of Things will ensure that ARPU will continue rising at 3UK as it delivers higher tonnages to customers?

No, again, for two reasons:

As mentioned above, other operators will both increase their network capacity and lower their cost bases so that they too can supply data at a lower price – in other words subscribers will continue to pay the same amount for more (as they have always tended to do). More data supplied will not translate into more revenue.

Data usage growth will slow. Just as voice minutes across fixed and mobile peaked (and then declined owing to substitution of other services), so data growth will reduce. Networks may be able to simultaneously supply the Smart Home with 7 different HD films, 8 different HD online games, 9 different news and information reports as well as carry the data from hundreds of home and personal sensors through virtualised network functions but humans only have one brain and can only cope with so much data. Greater speeds and bigger tonnages will suffer from diminishing marginal returns because human evolution won’t keep up with technology. And many of the machines that will be communicating with each other and carrying sensor information will not need huge quantities bandwidth and other network capabilities on a real-time basis – the demands on the network will stabilise compared with the massive growth we are currently experiencing just as the demand for steel girders, for example, has flattened.

Lessons from the steel industry: Network quality is unlikely to provide sustainable differentiation

High-cost US (and European) steel producers challenged by cheap foreign imports

The US (and European) steel industry suffered major disruption during the 1970s and 1980s as large quantities of steel started to be produced by economies with lower labour costs such as China, India and Korea. The major US steel producers – US Steel, National Steel and Bethlehem Steel – were massive companies which, in their heyday had each employed 100,000 people or more. They operated integrated steel mills. That is they mined the raw iron ore from their quarries, smelted it in a blast furnace and then refined the pig iron to produce steel which was cast into different products. The rationale for integration was that costs could be minimised by ensuring that low-value iron ore did not have to be transported long distances to the plant (which was built next to the quarry). However, even though they introduced efficiencies, they still employed large quantities of expensive labour during the process which pushed up their production costs relative to that in the emerging economies.

A low-cost start-up with a new business model

In the mid-1960s, Nucor, a medium-sized company with an extremely chequered history up to that point, purchased a steel joist manufacturer called Vulcraft. Unable to get favourable prices from American companies and concerned about the quality of imported steel, Nucor integrated backwards into steel production. Iverson, the Nucor CEO, established a new form of steel production in smaller plants, mini-mills, which melted scrap metal down to produce steel. These modern plants, which were located closer to destination markets to minimise shipping costs of the finished product were far more efficient than the old integrated mills. They used a fraction of the labour, producing a tonne of steel in around 45 minutes of labour time versus 3 hours at the integrated mills. This difference meant that by the mid-1980s Nucor could produce steel around 25% cheaper than the integrated mills. This, in turn, meant that not only could it beat its domestic rivals, but that it could also compete with competitors based in the cheap labour markets.

Quality (Repremiumization) does not result in higher prices

The companies with integrated steel mills were slow to react to the foreign threat and that of Nucor. Why? Because they believed in a form of ‘Repremiumization’ – that the quality of their steel was higher than Nucor’s and foreign competitors. Your author was an equity analyst in the 1990s for JP Morgan covering steel stocks and consistently heard the message from senior managers at US (and European steel operators such as British Steel, Usinor Sacilor and others) that their steel had higher tensile strength and was much higher quality than the cheap imports and steel produced by mini-mills. So, although they chipped away at costs they did not fundamentally re-engineer their businesses to match the cost base of the overseas players. The problem, of course, was that the steel provided by the foreign companies (and Nucor) was ‘good enough’ – it met the specifications required for the vast majority of applications. One customer put it like this when talking about the higher cost players, “They go on about the quality of their steel but it’s still carbon steel, it still rusts, so why should I pay so much more for so-called quality I don’t need?”

Low-cost wins

Today Bethlehem Steel and National Steel have gone (bankrupted in both cases) and US Steel, the biggest of the three, is grimly hanging on but producing less steel now than it did in 1900. Nucor, meanwhile, has grown to become a Fortune 300 company (see below). And as for the cheap foreign players? They have also thrived and Tata Steel and Mittal Steel together now own most of the European steel giants. The lesson here is clear: telcos cannot rely network quality alone as a means of differentiation, premium pricing and growth.

Figure 4: The importance of cost reduction in disrupted industries – The US Steel Industry

At best ‘repremiumization’ is misguided; at worst it is pandering to the hopes of some operators that they can somehow return to the ‘good old days’ of high margins and high market shares. Even the name suggests a return to nirvana. But the only time when European operators enjoyed premium pricing was before the market was liberalised – when the incumbents were state monopolies or duopolies. The moment that markets were opened up and competition ensued, so costs and prices were driven down. Higher ARPUs stemmed from higher volumes and premium services.

If operators want to differentiate and achieve higher ARPUs, revenues and margins in the increasingly tough saturated telecoms market of 2015 then service innovation – content services, enterprise services, enabling services – is the only solution. Otherwise the focus should be on cost reduction – building efficient and effective pipes.

If operators want to try to raise prices on the back of a repremiumization marketing message, that’s fine but they will enjoy as much success as King Canute had in ordering the tide back. One thing though, please don’t dress a misguided marketing pitch up as strategy – you’re fooling nobody but yourself.

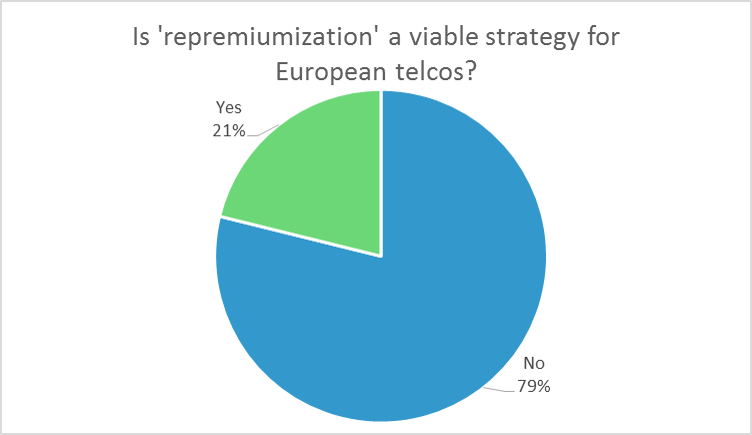

So that's our view, but what's yours? There's a snap poll below - we'll share the results on 16th July.

As at 15th July 2015, 79% of Respondents Agreed that Repremiumization is not a viable strategy for European Telcos

Source: STL Partners, n = 52

To access this 13 page Telco 2.0 Report in PDF format, including...

What is ‘Repremiumization’?

Promoted as a viable strategy recently at STL Partners’ Senior Executive Strategy Seminar in London…

…and put forward by a leading strategy house

Why is repremiumization 100% hogwash?

The argument simply does not stand up to scrutiny

Better networks are a source of advantage for operators by enabling cost leadership

Lessons from the steel industry: Network quality is unlikely to provide sustainable differentiation

Conclusions

...and the following report figures...

Figure 1: Where should the European telecoms industry place its bets for future success?

Figure 2: ARPU levels of 7 customer segments with and without better network services and digital ‘life experience’ offers

Figure 3: Sky UK winning market share and growing margins against the three bigger players

Figure 4: The importance of cost reduction in disrupted industries – The US Steel Industry

...Members of the Telco 2.0 Executive Briefing Service can download the full 13 page report in PDF format here. Non Members, please subscribe here. For other enquiries, please email / call +44 (0) 207 247 5003.

Technologies and industry terms referenced include: Authentication. Business Model, Digital Services, NFV, Repremiumization, SDN, Self-deception, Strategy, Telcos