Telco 2.0™ Research

The Future Of Telecoms And How To Get There

The Future Of Telecoms And How To Get There

|

Summary: In Q4 2012 Verizon was No.1 in Strategic Business Services (SBS) and had just bought a huge data centre provider. In Q4 2014, AT&T had overtaken Verizon in revenues from this segment. What happened, and what are the lessons for other telcos in the Enterprise SBS market? (May 2015, Executive Briefing Service, Cloud & Enterprise ICT Stream.) |

|

![]()

![]()

Below is an extract from this 22 page Telco 2.0 Report that can be downloaded in full in PDF format by members of the Telco 2.0 Executive Briefing Service and Cloud & Enterprise ICT Stream here.

For more on any of these services, please email / call +44 (0) 207 247 5003.

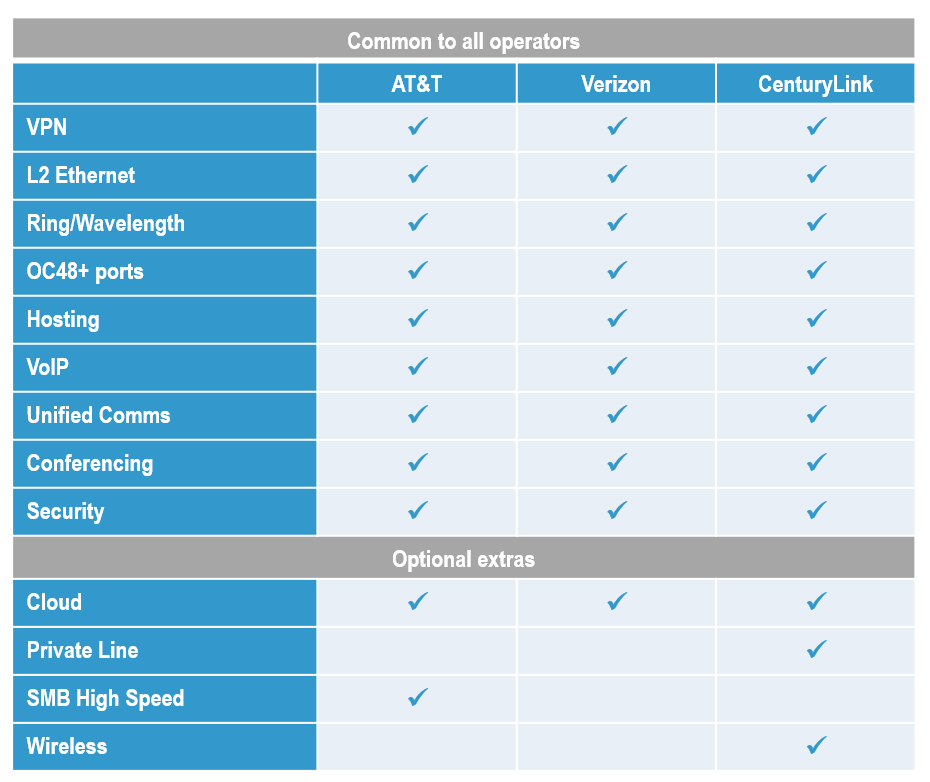

Since the beginning of the Telco 2.0 Transformation Index project, we have become aware that US operators are increasingly emphasising a new sub-segment, ‘strategic business services’ (SBS), usually carved out of their existing fixed-line or ‘wireline’ enterprise operations. Typically, strategic business services includes the newer and supposedly higher-growth products, such as cloud computing, dark fibre or wavelengths, Ethernet VPNs, machine-to-machine mobile (although not always), security services, and Voice 2.0. There is no standard definition, and comparisons across carriers are therefore complicated. We prepared the table in Figure 1 for the first wave of the Index in Q4 2012 – since then, AT&T has made it clear that cloud is included in its definition.

Source: Telco 2.0 Transformation Index

The story usually runs as follows: “although the wider enterprise or business wireline segment is stagnant or shrinking, the strategic services sub-segment is growing fast, offers higher margins and has lower-churn customers, so that’s the bit you should be looking at.”

US fixed operators have substantial customer bases in the SMB and enterprise space, who are typically taking “legacy” services like T-carriers (high speed data links based on TDM technology) or shared web hosting. As the cloud develops, these customers are becoming available to a new set of competitors from the IT industry – e.g. Microsoft Azure or HP – and from the Web 2.0 industry – e.g. Amazon Web Services, Rackspace, or Google. Further, some historic ISPs have intensified their efforts to sign up end-customers, like Level(3) or Zayo (ex-Abovenet). The challenge for the telcos is to move these customers onto more modern products without spilling them to the competition. As a result, the SBS segment is indeed a real indicator that needs watching.

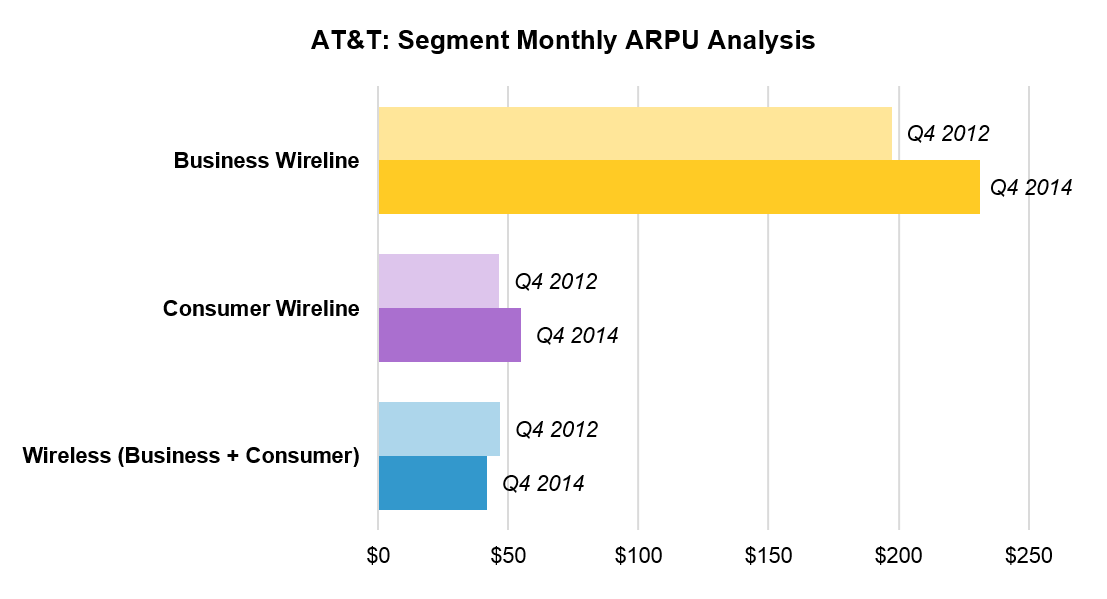

Another reason that it’s important is that the US telcos’ business customers are typically very big spenders. In Self-Disruption: How Sprint Blew It, we showed that SMB users were typically very important indeed to Sprint, and that their failure to attend to their needs around the shutdown of Nextel and migrate them effectively to a suitable alternative tipped Sprint into a crisis it has yet to recover from. The following chart shows monthly average revenue per user (ARPU) for AT&T’s three major operating segments. Note that ‘Business Wireline’ corresponds to AT&T’s ‘Business Solutions’ reporting line. Business Wireless is included in ‘Wireless’.

Source: Telco 2.0 Transformation Index

Note: ARPU is also known as ‘Average Revenue Per User’. Here, a ‘user’ is defined as a wireless or wireline connection, or ‘revenue generating unit’.

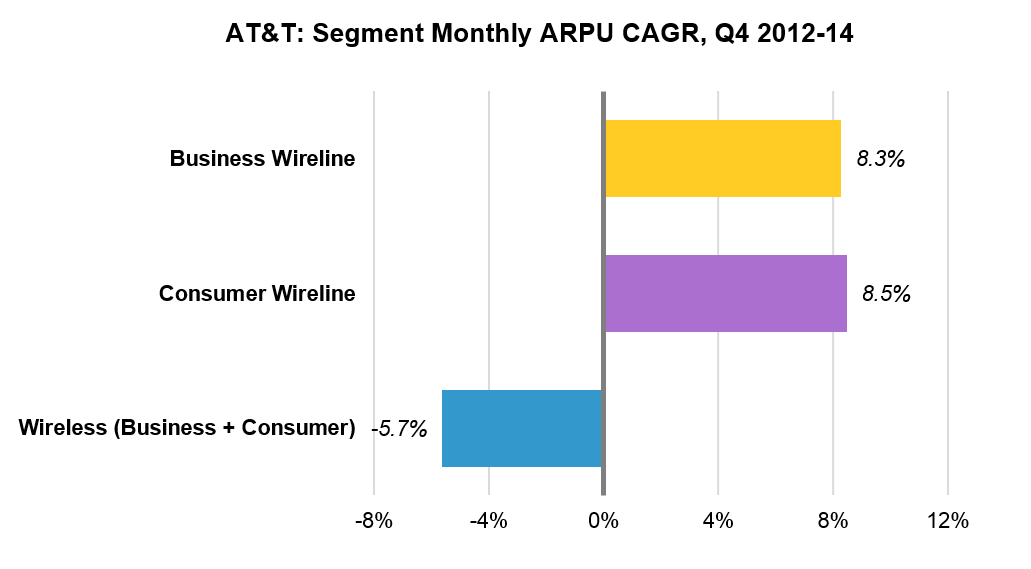

As Figure 2 shows, AT&T’s business customers spend several times more on average (per connection) than wireless, usually considered to be the jewel in the crown, and consumer wireline. Of course, this in part reflects that a considerable portion of AT&T’s enterprise revenues are generated by services beyond telephony, business broadband and video (the denominator) – even if many customers for these additional services will also purchase one or more of its core products. Some of these services fall within AT&T’s ‘strategic business services’ reporting line. Figure 3 shows growth over the last two years, and that Business Wireline managed to grow its ARPU 8.3%, while wireless began to feel the impact of the US price wars.

Source: Telco 2.0 Transformation Index

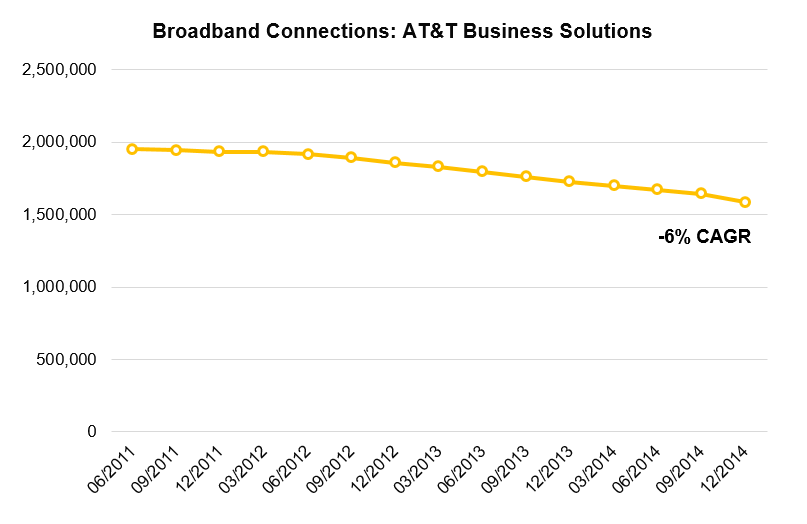

However, the performance in terms of ARPU owes something to the fact that AT&T lost a significant number of less-attached and lower ARPU customers. The next chart shows the drop in business broadband connections over the last three years.

Source: Telco 2.0 Transformation Index

The key competitor here is cable. Cable operators have dramatically increased their business services revenue recently, and have been offering very attractive pricing on symmetrical broadband, very often using extension drops from their fibre distribution networks. They have also been offering very keen pricing on voice (still a key product for businesses) and WLAN, and using some novel technical options to extend their Ethernet footprints.

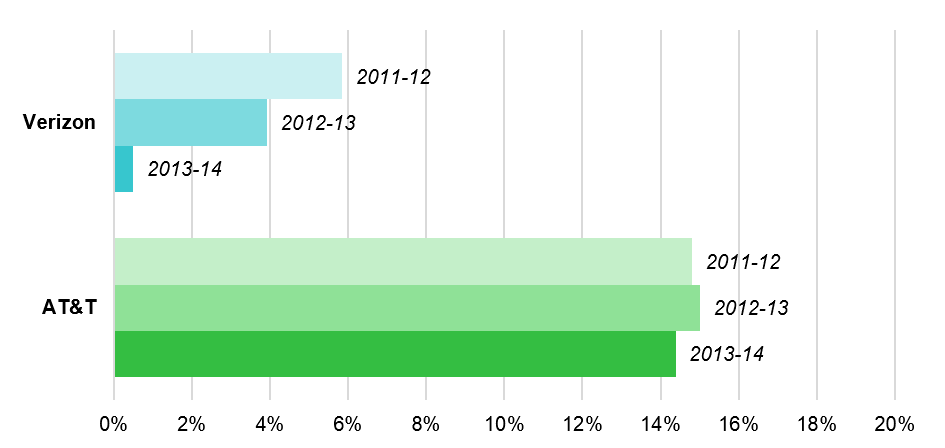

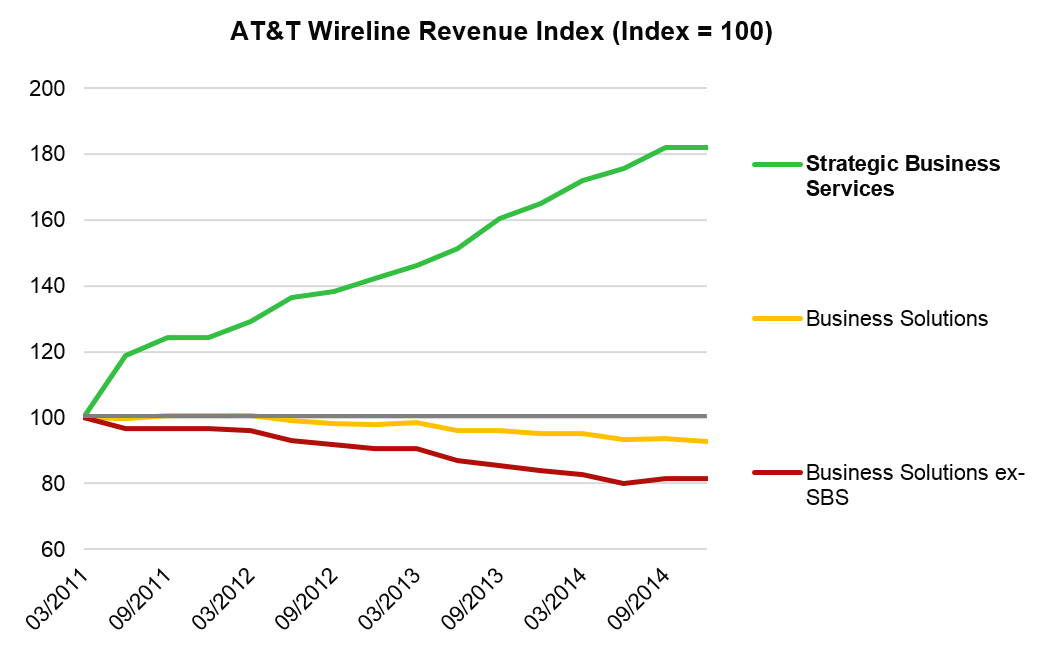

As a result, the underlying performance of Business Wireline and its sub-segment, Strategic Business Services, was dramatically different. This is shown in Figure 5 below:

Source: Telco 2.0 Transformation Index

The challenge even for successful carriers in SBS is that a relatively small line of business has to scale up fast enough to make the much bigger enterprise segment grow. This poses significant challenges in terms of management. It is at least preferable, though, to the alternative – no growth in SBS, or indeed anywhere else in the enterprise segment.

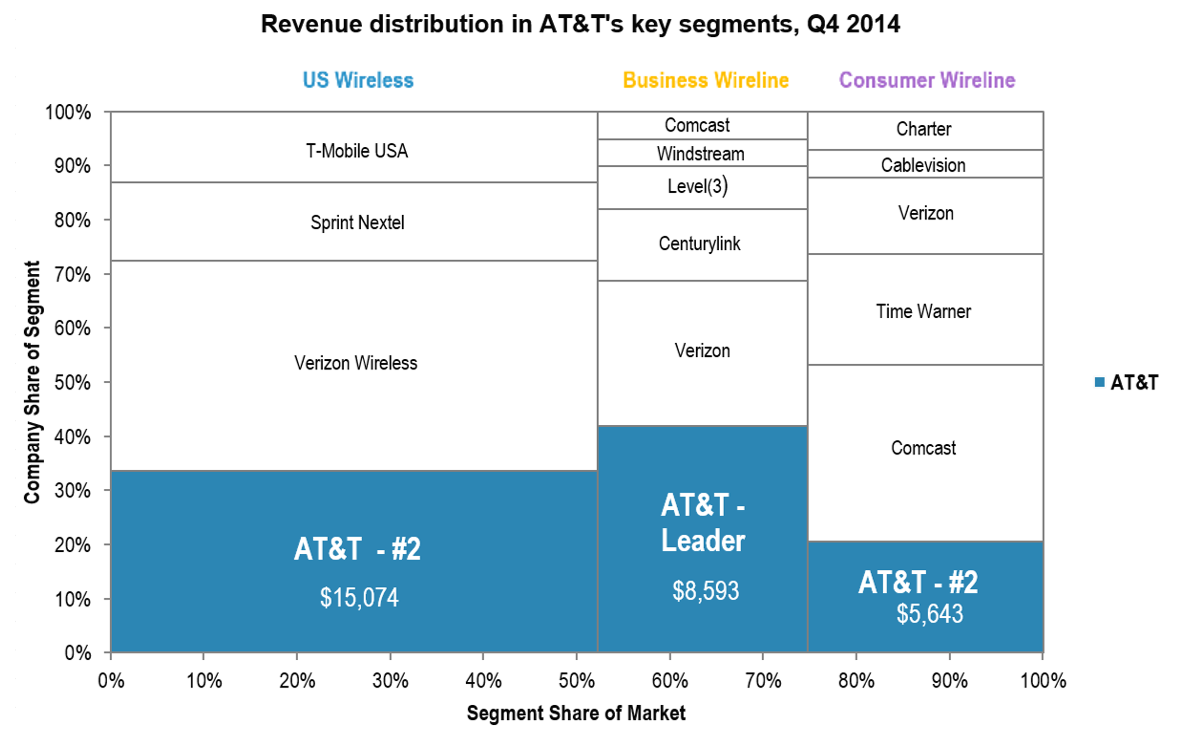

Unlike in consumer wireline, AT&T and Verizon compete coast-to-coast in business wireline. AT&T is the market leader and Verizon is no.2, as the next chart shows. Verizon leads in wireless, where AT&T is no.2, the mirror image of the position in business.

Source: Telco 2.0 Transformation Index

In the first wave of the Transformation Index, we noted that Verizon had just finished a reorganisation that created a new division, Verizon Enterprise Services (VES), regrouping all their SBS activities and all their industry vertical products. They had also just closed the acquisition of Terremark, a major operator of data centres. We therefore had some confidence that they might do well, even if AT&T was showing signs of improving its SBS offering significantly, taking an interest in developers, deploying a new and much stronger M2M platform, and diversifying its suppliers and technology partners via the Domain 2.0 programme.

So, what happened?

To access the rest of this 22 page Telco 2.0 Report in full, including...

...and the following report figures...

...Members of the Telco 2.0 Executive Briefing Service and Cloud & Enterprise ICT Stream can download the full 22 page report in PDF format here. Non Members, please subscribe here. For other enquiries, please email / call +44 (0) 207 247 5003.

Technologies and industry terms referenced include: Amazon, AT&T, business services, carrier Ethernet, CenturyLink, cloud, colocation, differentiation, Domain 2.0, enterprise, FiOS, hosting, innovation, IP-VPN, Level(3), Project VIP, SaaS, Savvis, SBS, SDN, SMB, strategy, telecoms, Terremark, Verizon.