Telco 2.0™ Research

The Future Of Telecoms And How To Get There

The Future Of Telecoms And How To Get There

| Summary: It was exhilaratingly clear at the Silicon Valley Brainstorm, March 27-28 2012, that critical inflection points are being reached in many key areas of the digital economy: the challenges are increasingly well defined, and the intellectual, practical and economic resources being employed to solve them have the quality, power and resources to succeed. The tantalising question for all was “how do we position ourselves and implement strategies that will enable our business to be one of those to profit from (or at least survive) these changes?” Our top-level take-outs from the event. (March 2012) |

|

Introduction

An international group of 225 senior executives, entrepreneurs, academics and policy influencers from across the communications, media, retail, banking and technology sectors met at the New Digital Economics Silicon Valley Executive Brainstorm in San Francisco in March 2012. The brainstorm was part of a research and industry transformation programme from business model innovation firm STL Partners. Supported by leading trade bodies, the Executive Brainstorms are held on a regular basis in different parts of the world to bring together business leaders and strategists to think creatively about new growth opportunities.

Each event builds on the output of the previous one and integrates cutting-edge research, case studies and analysis from leading players. The events use a unique and widely acclaimed interactive format called ‘Mindshare’ to help clarify the important ‘next steps’ for both individual companies and industries.

The theme of the event was ‘New Business Models and Growth Opportunities in a Hyper-Connected World’, and it comprised four inter-connected one-day brainstorms covering ‘The Digital Economy 2.0’, ‘Digital Commerce 2.0’, ‘Digital Entertainment 2.0’ and ‘Digital Things 2.0’ (Agenda remider). The rest of this page summarises our top level impression of the brainstorm and key next steps. We will publish detailed reports of the sessions next week.

Visceral Impression: a sense of change

The Silicon Valley brainstorm was particularly exciting because it truly felt like a catalyst for productive change, rather than just another conference, just another opportunity to share and reflect on the status of the market and disruptions to it. We put this down to the event's focus on the most pertinent questions, the quality of the stimulus material prepared and presented and, not wishing to be immodest, the improvements we’ve made to the event's brainstorming processes which generated a higher level of energy from a wonderful crowd of open-minded senior execs from multiple converging industries. We are really looking forward to take it a step further at the EMEA Brainstorm in London on 12-13 June. In the meantime, this two minute video gives a good sense of the energy and progress we saw in San Francisco.

To set the scene, some of the main changes in the digital economy that we explored through analysis and debate were:

In overview, there was one seeming over-riding certainty: what can happen, will happen. The uncertainties are now principally in when, how and where will these changes take place first, and which companies will be equipped and position to profit from them.

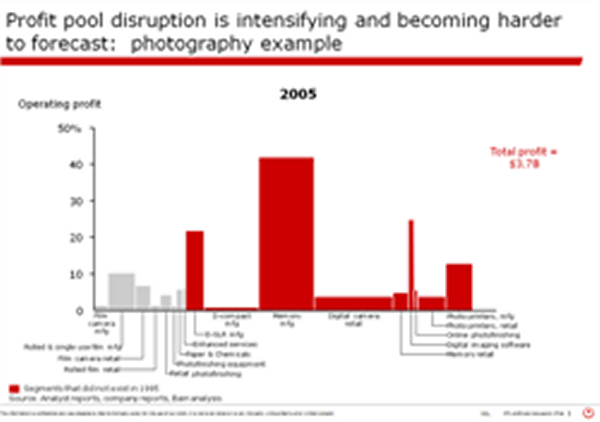

The scale and pace of change and the uncertainties of the future can seem perplexing, but analogies with other industry disruptions can show that these transitions are not unique. Jennifer Binder Le Pape from Bain described the transition of the digital photography industry between 1995 and 2005, showing how dramatically profits moved from incumbent players who failed to adapt to the changes to digital disruptors. The first chart shows the $1.9Bn 1995 profit pool dominated by film and photofinishing.

The second chart shows the $3.7Bn 2005 profit pool dominated by memory manufacturing.

With the benefit of hindsight it’s relatively easy to understand the transitions that happened in photography, and most in 1995 understood the nature if not the scale of the impact of digital technologies. Of course, even further changes have come since 2005, and just this week Facebook has spent $1 billion on Instagram – yet another disruption in history of photography, which might now be described as a feature of other digital products.

Over and above the detail and definitions of the changes in photography, the key points are a) that major changes can and do happen in industry profit pools, and b) despite the foreknowledge of coming change, few if any were able to map the complete shape of this transition out accurately in advance. This challenge faces many other industries today.

One of the factors that make the future difficult to predict is that the digital economy comprises many inter-related ecosystems and platforms, including: communications, cloud and device computing, content creation and aggregation, payments, advertising and marketing.

Major changes can arise in a number of different ways, each with their own challenges. For example, Apple and Google created entirely new platforms of massive scale. These single player disruptive innovations are rare, partly because they are so difficult to achieve, and partly because most players don’t have the market position to do this. Most players need different approaches to drive innovation. Some leading players can catalyse a market by creating a de facto standard that others join (e.g. Adobe and PDF), while others innovate on the back of broader collaboration through standards (e.g. SMS). None of these approaches is guaranteed to work.

A major Telco 2.0 report previewed at the event that we will be publishing next week outlined the different strategies available to telcos looking to build new business models, as well as the different attitudes and approaches of executives across the value chain – from telcos through to vendors and ‘upstream’ industries such as media and entertainment (email to pre-register). The report outlines the different possible strategies shown below, and we are working on a number of projects and pieces of analysis that explore the opportunities to drive issues forward and which we will share more on throughout the year.

We are working on a number of initiatives to help lubricate the ecosystems and the creation of new sources of value that legitimately empower and protect end-customers, as well as creating new business opportunities.

STL Partners will also be driving new research and communities to support strategists in: Digital Commerce (advertising and payments), Digital Entertainment (TV, film, media and publishing); Digital Things (M2M and embedded); and Cloud 2.0 (market evolution, telco strategies and role in Telco 2.0).

We believe that because of the complexities and inter-relationships between the ecosystems, it’s useful for participants in the different work streams to maintain a dialogue and establish understandings with participants in the other streams as well as their own. This is what we aim to achieve in our global regional brainstorms, such as the Silicon Valley event just gone, as well as sharing the latest thinking and practice in business model innovation.

To join the next Brainstorm in EMEA in London on 12-13 June, or subscribe to our ongoing research programme, please email or call +44 (0) 207 247 5003.