|

In 2011 we’ve really been struck by the ‘can do’ attitude of companies in the Middle East and Asia Pacific regions towards Telco 2.0 strategies, and their desire to leapfrog legacy (Western) business models and technologies. This was highlighted at the New Digital Economics & CSG APAC Executive Brainstorm in Singapore, as were increasing similarities between APAC region business model challenges with those in Europe and America. (December 2011, Executive Briefing Service, Transformation Stream.) |

|

Below is a preview of the first section of analysis from the Brainstorm covering core Telco 2.0 strategies. Further analysis (on Mobile Broadband, Mobile Money, Customer Experience, Digital Entertainment, Apps & HTML5, and 'Dealing with the Disruptors'), will be published in the coming weeks for members of the Telco 2.0 Executive Briefing service and for event participants. Non-members can subscribe here or for other enquiries, please email or call +44 (0) 207 247 5003.

To share this article easily, please click:The New Digital Economics Executive Brainstorm and CSG APAC Executive Forum, 30th November – 1st December 2011, was held at the Capella Resort, Singapore, and explored the nature of the fast changing ‘digital economy’ and telcos’ strategic options and tactical opportunities to respond to it.

The two day interactive event enabled 100 specially-invited senior executives from across the communications, media, payments, internet and technology sectors to focus on strategies that accelerate new growth opportunities and business model innovation.

It used STL Partners’ unique ‘Mindshare’ interactive format to help participants walk away with actionable ideas for new business growth. This involved cutting edge market analysis from STL Partners and the Telco 2.0 Initiative, case studies and use cases from CSGI, round table discussions, panel debates and interactive voting using on-site collaborative technology. It also included an Innovation Showcase to bring to life some of the concepts under discussion.

The aim was to facilitate the exchange of best practices, experiences, strategies, business approaches, challenges and visions within the theme of Accelerating New Growth Opportunities in Telecoms, Media & Technology. The Brainstorm was sponsored and co-hosted by CSG International.

84% of APAC participants believed that ‘Telco 2.0’ strategies – leveraging assets to create new B2B and B2B2C services and more sustainable business models (see Telco 2.0 Strategy: New Growth needs New Metrics) - were either already important or would soon be important to their organisation (see Figure 1 – Senior management attitudes to Telco 2.0 Strategies).

Figure 1 – Senior management attitudes to Telco 2.0 Strategies

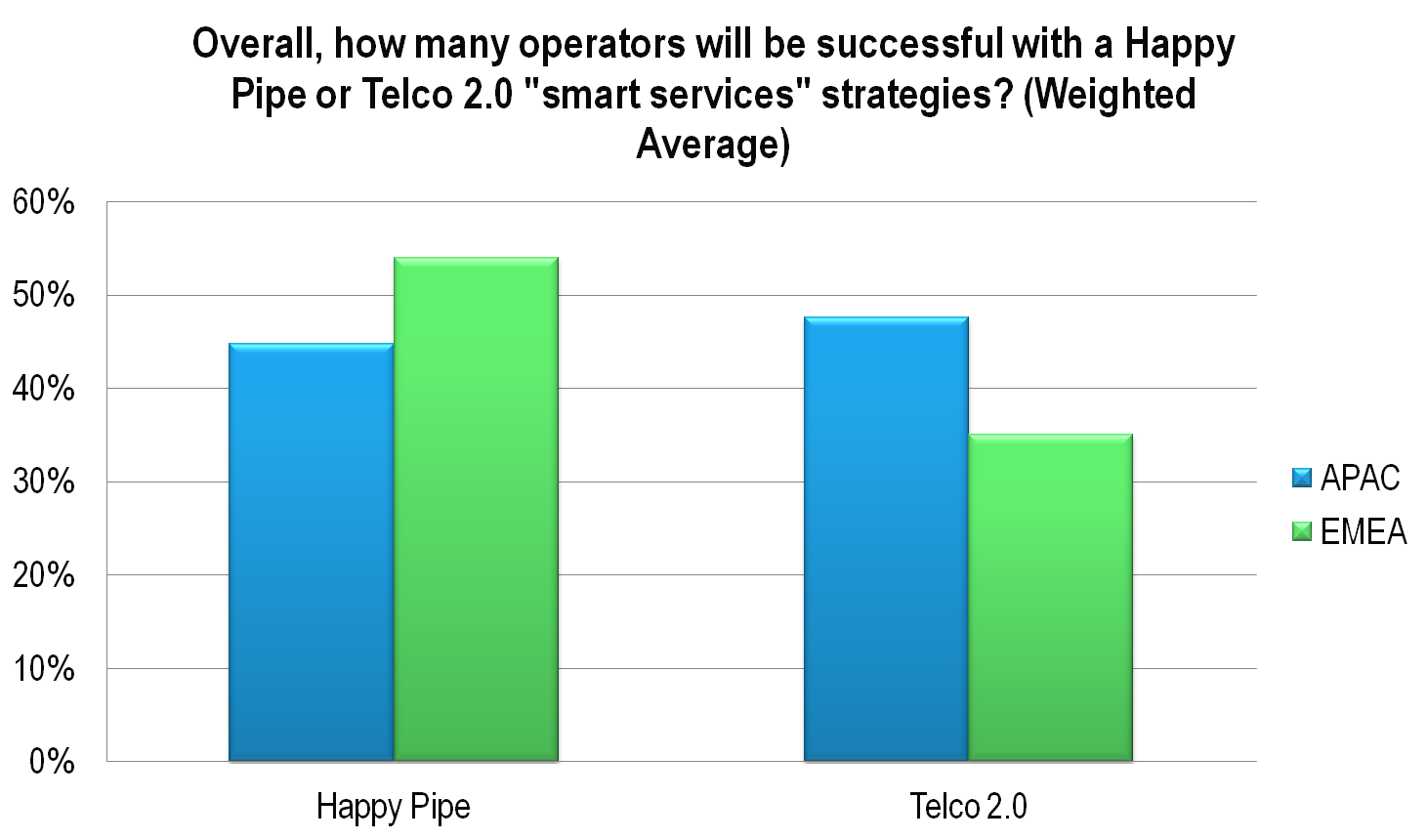

Delegates also voted on the likely success of two key Telco 2.0 strategies (see Figure 2 – APAC and EMEA views on ‘Telco 2.0 Happy Pipe’ and ‘Telco 2.0 Full Services Strategies’):

Figure 2 – APAC and EMEA views on ‘Telco 2.0 Happy Pipe’ and ‘Telco 2.0 Full Services Strategies’

The challenges facing operators in the region are very similar to those faced in EMEA and the Americas, with a wide concern for flat-lining revenues in developed and emerging economies, which the majority of attendees represented.

Figure 3 – Pressures on the core business model

Telcos have become popular stocks for investors recently, with their considerable cash flows and good dividends, although investors are wary of telcos’ when they start to discuss innovation for fear that it will diminish returns.

Investors understandably want telcos to raise data prices, reduce costs, and re-organise for maximum agility and ability to enable others. Telco 2.0 agrees with these themes, but believes telcos can go further and do better making these changes in such a way that they enable new business models.

We believe that 2011 has been a watershed year for Telco 2.0 business model innovation, although the progress we’ve seen has not always been exactly how we envisaged back in 2006. Key differences are that many of the innovative ‘two-sided’ type business models we see in operation are:

Telco 2.0 / STL Partners will:

The rest of this report, to be published next week, summarises the findings and next steps resulting from the Brainstorm, covering:

Non-members can subscribe here or for other enquiries, please email / call +44 (0) 207 247 5003.